Come, lets SCALE the business together..

One BD Template, Five Segments: A Blueprint for Winning Market Share in India's Footwear Industry

When BD is your strategy

Ashmeer M Sayyed

7/16/20265 min read

One BD Template, Five Segments: A Blueprint for Winning Market Share in India's Footwear Industry

How a multi-format footwear house can turn one retail expansion playbook into a five-year, portfolio-wide growth engine — without a single rupee figure that gives away who this is about.

India's footwear and sportswear industry is one of the more crowded, capital-hungry categories in retail — a multi-thousand-crore market compounding at 20–25% a year, chased by every player from global giants with hundred-plus-store networks to homegrown challengers still finding their shelf space. In a market like that, most brands make one strategic choice and live with it: go mass and chase volume, or go premium and chase margin.

The client at the centre of this case study made a different bet. It is a house of brands — a single retail parent that owns a relaunched heritage sportswear brand, holds an exclusive multi-geography license for a global performance brand, has a celebrity co-founder anchoring a third label, and runs an experiential big-format outlet business alongside a value-tier multi-brand network. Five distinct consumer segments, five different price points, one balance sheet.

That's an unusually complex retail engine to build in five years. It only works if there is one repeatable, disciplined Business Development (BD) Template running underneath all five formats — because the moment BD execution becomes format-by-format improvisation, capital gets wasted on the wrong sites, franchisees get mismatched to the wrong brand, and formats start cannibalising each other in the same catchment.

This is the story of that template — what it is, how it's applied differently across five very different segments, and what a five-year, market-share-first strategy looks like when it's built store by store rather than slide by slide.

The Business Development Template: One Engine, Five Formats

At the core of the plan sits a five-stage, standardised site-to-store process, designed to compress the industry-typical letter-of-intent-to-launch timeline down to roughly 90 days:

1. Market Screening — catchment mapping, competitive density, and rent benchmarking against a priority city list specific to each format, not a generic national list.

2. Site Shortlisting — field visits, format scorecards, co-tenancy mix, and an anti-cannibalization check against every other format already operating in that micro-market.

3. Commercial Negotiation — a hard floor of rent under roughly 12% of projected revenue, a minimum five-year lease, and a built-in exit clause at year three to cap downside on unproven locations.

4. Legal & Compliance — lease execution, trade license, fire NOC, and franchise agreement, run in parallel rather than sequentially.

5. Store Launch — fit-out, visual merchandising, staff training, and a coordinated launch activation.

The template doesn't change from format to format — but the inputs into each stage do, and that's the design discipline that makes a five-segment portfolio investable rather than chaotic. A 600–1,000 sq. ft heritage-brand EBO in a Tier-2 cricket-belt town is screened, negotiated, and launched on the same five stages as a 25,000–35,000 sq. ft experiential flagship in a metro mall — but the site criteria, the negotiation leverage, and the launch playbook underneath each stage are format-specific.

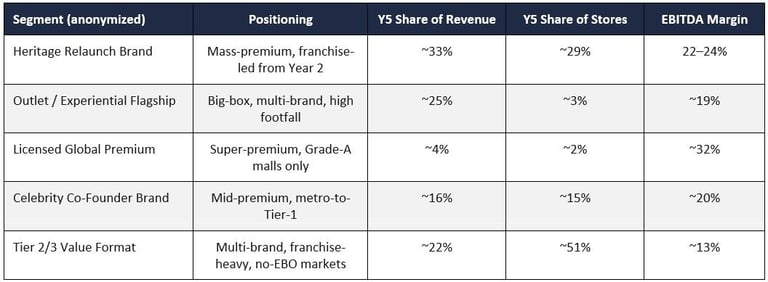

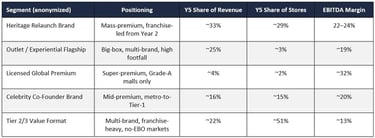

The Five-Segment Portfolio: Same Template, Five Very Different Economics

Here's where the anonymized numbers get interesting. Each segment was mapped against its own unit economics, margin profile, and role in the portfolio — and the differences are the whole point of a house-of-brands strategy.

The single most useful insight in the entire model sits in that table: the outlet/experiential format carries roughly 3% of the store count but generates roughly a quarter of portfolio revenue. It's the highest revenue-density format in the network by a wide margin — a handful of large-format, high-footfall stores doing the work of dozens of small ones. That's not an accident; it's a deliberate portfolio-construction choice, and it's the kind of insight a BD strategy has to surface before capital gets allocated, not after.

At the other end, the value-tier multi-brand format carries over half the store count but a fifth of the revenue — its job isn't margin, it's market share and geographic reach into Tier-2/3 towns no single-brand EBO could justify entering on its own. Lower EBITDA (~13%), but it's the format that converts “underserved aspiration” in smaller cities into an actual sales network, and it protects the flanks of the higher-margin formats by capturing demand the EBOs can't reach.

The licensed global premium format is the outlier by design: smallest in both store count and revenue share, but by far the highest margin (~32% EBITDA). Its role isn't scale — it's brand halo and a proof point that the portfolio can compete at the very top of the market, in Grade-A locations most challengers can't access at all.

Anti-Cannibalization: The Rule That Makes Five Formats Coexist

Running five formats under one balance sheet only works if they don't compete with each other for the same customer in the same catchment. The BD template enforces this with hard, contractual geographic rules — not soft guidelines:

• A minimum exclusion radius around every brand-dedicated store, inside which the value-tier multi-brand format cannot open.

• A wider exclusion radius around the outlet/experiential flagship, since its footfall draw is metro-wide, not hyperlocal.

• Franchise agreements that explicitly bar a value-format operator from opening a competing single-brand store without written consent.

• Monthly revenue monitoring — if an adjacent store's sales drop meaningfully after a new opening, the format boundary gets reviewed.

This is what separates a portfolio strategy from just running five brands in parallel: the formats are built to feed each other's brand equity — the mass entry point building awareness that the premium format later monetizes — rather than quietly eating each other's sales.

The Five-Year Arc

Modelled conservatively, the portfolio's revenue scales roughly 13x from Year 1 to Year 5, while the store count grows roughly 9x — meaning revenue per store improves meaningfully as the network matures, not just as it gets bigger. Blended EBITDA margin expands from roughly 12% in Year 1 to roughly 20% by Year 5, profitability turns positive by Year 3, and free cash flow turns positive by Year 5 — the point at which the franchise-led formats are throwing off enough cash to fund their own next phase of expansion without fresh capital.

None of that happens without the underlying BD discipline: a single, repeatable site-to-store engine; format-specific economics modelled honestly rather than optimistically; and hard anti-cannibalization rules enforced in every franchise contract from day one.

Why This Matters Beyond One Client

The lesson generalizes well beyond footwear. Any brand house sitting on multiple formats — owned, licensed, celebrity-backed, or value-tier — faces the same underlying problem: growth targets get set at the portfolio level, but execution risk lives entirely at the site level. A BD Template that's disciplined enough to flex across five different unit economics, while staying rigid on process, margin floors, and exclusion rules, is what turns a five-format ambition into a five-year, market-share-gaining reality instead of five brands quietly competing with themselves.

AsRaVe (Associated Retail Venture Pvt. Ltd.) advises apparel and footwear brands on franchise expansion, EBO/FOFO rollout strategy, and multi-format portfolio design across the Indian retail landscape. Get in touch to discuss a BD strategy for your brand's next phase of growth.

Office

14/2, Sarjapur Road, Bengaluru, 560035